Rising military tensions between India and Pakistan could shift markets quickly. From defence manufacturers...

Discover why long-term investing outperforms market timing, with real examples, data insights, and simple...

Struggling with debt? This guide breaks down two proven strategies, Snowball and Avalanche, and includes...

Learn how compound interest builds wealth with real-life examples and a 10% return scenario. See how...

Looking for easy, tax-free income? The UK’s Rent a Room scheme lets homeowners earn up to £7,500 per...

Looking for flexible income as a new mom? This guide offers 10 legitimate ways to make money from home,...

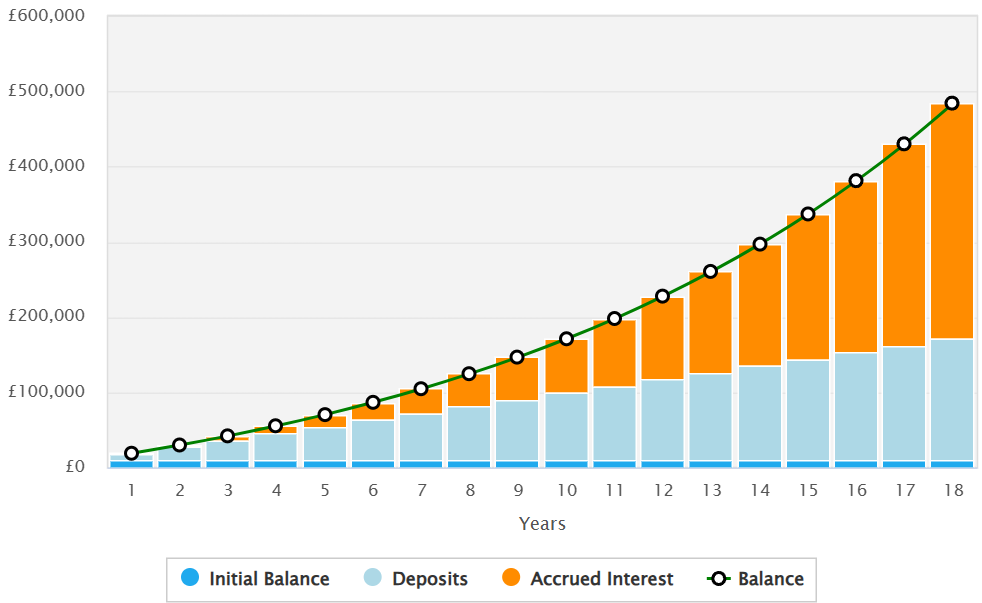

If a parent contributes the maximum to a Junior Stocks & Shares ISA and an NS&I Premium Bond account,...

Junior ISAs are tax-free savings and investment accounts for children in the UK. Learn how they work,...

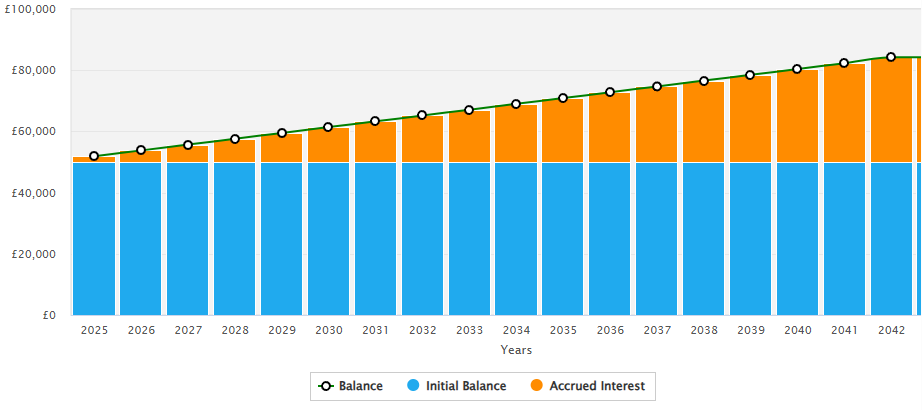

NS&I Premium Bonds offer a unique way to save money in the UK. With no interest, you can save up to £50,000...

Discover how Student Finance works in the UK for 2025, including tuition fees, maintenance loans, application...